Monthly Market Rollup: March to April 2024

Economic slowdown vs. Inflation in an election year puts the Fed on the back foot against Fiscal giveaways. How will the Fed cut when Inflation picks up and political giveaways abound?

Hello again to our Monthly Market Rollup for the end of March 2024. We aim to send out these chart heavy market summaries at the turn of each month. Please be aware that these notes are not investing advice and should be enjoyed as entertainment and for informational purposes only. Always do your own research. Sources can be found below each graphic.

As usual, we divide these monthly notes up into an Economic watch currently focused on the potential for a Recession, an Inflation section, and a Fed focused section, along with a Conclusion. Enjoy!

Recession Watch:

Numerous economic areas in the US market still are pointing towards a potential Recession.

A majority of the U.S. States have entered Recession territory already:

Source: https://x.com/GameofTrades_/status/1770850472590451053

Which is in line with a decline in Small Business Net Hiring Plans:

Source: https://x.com/Lvieweconomics/status/1767531892209795293

Chapter 11 Bankruptcy filings are increasing:

Source: https://x.com/GameofTrades_/status/1771522288258613258

Trucking employment continues to deteriorate:

Source: https://twitter.com/GameofTrades_/status/1766811243107770527

And permanent job losses continue to look Recessionary:

Source: https://x.com/GameofTrades_/status/1765724082597924925

However, some aspects of the Economy are experiencing rapid declines following dramatic run-ups during the Covid years:

Median home prices, for example:

Source: https://x.com/GameofTrades_/status/1774451607037497764

And Domestic Year-over-Year (YoY) Income:

Source: https://x.com/GameofTrades_/status/1771246717331206266

So while much of this could be mean reverting back to normal in a post Covid environment, there’s a sufficient breadth of deterioration to give reason for concern.

Inflation Watch:

Turning to Inflation, as we’ve been noting for a few months, inflation seems ready to pick up in the coming months:

From the correlation with Copper:

Source: https://twitter.com/FrancoisTrahan/status/1770094470547038558

And from International freight rates which look ready to recover:

Source: https://twitter.com/AndreasSteno/status/1772893722079801504

How bad could the inflation get?

Well, here is the current environment overplayed on the 1970s, which is interesting to look at if nothing else.

(The current inflation numbers on the left hand side, and 70s inflation numbers on the right hand side.)

Source: https://x.com/GameofTrades_/status/1770457808837775751

So Inflation returning seems like a high likelihood.

Federal Reserve Watch:

Where does the Fed go between these two nightmares (Economic Recession and Inflation)?

Simply put, I think it stays flat for a longer period of time than expected.

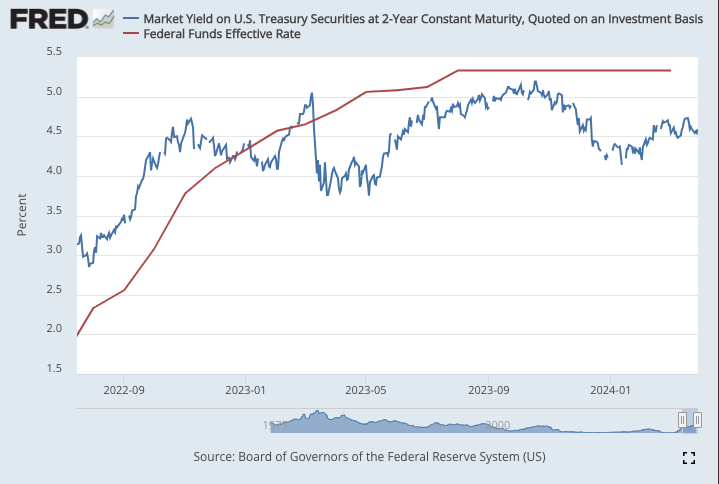

In previous notes we’ve shown how the 2 year is often a directional predictor of where the Fed will send short term rates, but even the 2 year seems unable to make up its mind about where to go at the moment:

Source: https://fred.stlouisfed.org/series/DGS2

That right edge of the chart is a bit hard to see so let’s zoom in:

The 2yr dropped into January of this year, but has rebounded almost 50 basis points since then. Does the 2yr revert to the Fed Funds, or will the Fed eventually capitilate?

Conclusion:

Numerous indicators all continue to be blink red with the potential for a Recession. Part of the Economy and a majority of U.S. States appears to already be in Recession already. However, the market hasn’t rolled over yet, so the question remains: ‘what is really happening’?

One of the more interesting answers I’ve heard recently is that the dramatic addition of energy production within the U.S. over the last few years, coupled with the ongoing re-shoring and near-shoring of supply chains will lead to a dramatic rebound in US employment as our manufacturing sector grows rapidly over the next few years. And the market is already anticipating all this.

My view is not so optimistic for labor growth.

In my view, the easiest answer is the precarious position of the U.S. Dollar, its ongoing debasement, and the resulting market’s ability to prolong these frothy equity valuations in the face of deteriorating Economic news.

We find ourselves in a rare moment that seems primed for Stagnation. Crypto, Gold, Nvidia, Bonds, and Commodities all are signaling that an Inflationary regime is in effect and a whipsawing volatility reigns (Cocoa prices, anyone?).

As we’ve been saying for months now, the Fed is going to get itself stuck between the coming wave of re-flation, and a deteriorating Economy. And for the Fed, the easiest thing to do will be to emphasize the role of the Fiscal side of government and stand pat.

Three rate cuts this year? I’ll take the under.

There’s still a potential for the wheels to fall off the Commercial Real Estate Market and/or for regional banks to have a problem, but with the 2yr now going back higher on rates we seem mired in a yield curve that enjoys being inverted. And he Recession won’t land until that Yield curve de-inverts.

How long will a yield curve stay inverted? I guess we will all find out together.

Until next month.

Please subscribe if you haven’t already and consider our Pro Tier if you would like direct on-demand access to my entertaining views on the Economy.